Last night, Treasurer Jim Chalmers handed the federal budget that focused on economic growth, job creation, and investment in infrastructure and services. With the biggest turnaround on record and the first surplus in 15 years, it has certainly made the Government look good. We go beyond the black and outline our key highlights allowing you to see what it means for you.

Our key takings are:

- Payday Super

- Future earnings for super balances above $3m taxed at 30% from 2025-26

- $1,500 low and middle-income tax offset ends

- $20k immediate asset and small business energy incentive

- Strengthening of medicare

- Incentives to improve residential rental property supply

- Access to home guarantee scheme expanded to friends and siblings

Individual tax rates

There is no change to the planned stage three of tax cuts legislated to come into effect next year.

The stage-three tax cut will remove the 37% tax bracket, decrease the 32.5% tax bracket to 30% and increase the threshold for the top tax bracket from $180,001 to $200,001.

It is expected to cost the budget $69 billion over the next four years.

Pay-as-you-go (PAYG) and Goods and Services Tax (GST) payments

To assist small businesses operating on wafer-thin margins, the budget introduces a new way of calculating the increase of Pay As You Go (PAYG) and Goods and Service Tax (GST) payments.

At present, the 12% GDP adjustment factor will be halved with a new 6% rate, a move designed to improve cash flow for over 2 million small businesses.

Payday Super

From 1 July 2026, employers will be required to pay their employees’ super at the same time as their salary and wages.

Superannuation guarantee (SG) payments will be made on paydays, which means that employers will need to ensure they have systems in place to make these payments regularly and on time. This may require changes to payroll processes and potentially increased administrative costs for businesses.

For employees, this change could mean a more regular and consistent flow of superannuation contributions into their retirement savings accounts. It may also mean that employees need to be more aware of their superannuation entitlements and monitor their superannuation accounts to ensure that payments are being made correctly and on time.

As a result, the federal government estimates a 25-year-old earning average wages will be roughly $6,000 better off at retirement.

Future earnings for super balances >$3mil taxed at 30% from 2025-26

From 1 July 2025, an additional 15% tax on earnings will apply to members with superannuation and pension balances above $3 million.

The additional 15% tax will apply to ‘unrealised gains’. This will mean that tax liability will arise if the value of fund assets increases even if they are retained.

At present, all income is taxed at either 15%, or 10% for capital assets that have been held by the fund for more than 12 months. Unrealised gains, that is gains that are made because of changes in value, are not currently taxed – tax only applies when the gain is realised on the sale or disposal of the asset. This measure is expected to eventually recover an additional $2 billion a year for the government.

$1,500 Low and Middle Income Tax Offset (LMITO) ends

The Government has confirmed that they will not extend the $1,500 Low and Middle-Income Tax Offset beyond 2021-22.

Originally announced in the 2022–23 Federal Budget, the LMITO was increased by $420 (a one-off $420 cost of living tax offset) for the 2021–22 income year. This increased the base amount to $675 and the full amount to $1,500.

$20,000 small business energy incentive

The Government has committed to a Small Business Energy Incentive Scheme that offers a bonus tax deduction of up to $20,000; meaning up to $100,000 worth of spending will be eligible for the incentive.

The Small Business Energy Incentive encourages small and medium businesses with an aggregated turnover of less than $50 million to invest in spending that supports “electrification” and more efficient use of energy.

Eligible assets or upgrades will need to be first used or installed ready for use between 1 July 2023 and 30 June 2024 to qualify for the bonus deduction.

Instant asset write-off

The $20,000 instant asset write-off for small businesses will continue until 30 June 2024, allowing businesses to deduct the full cost of assets up to that price that were installed or ready for use before that date.

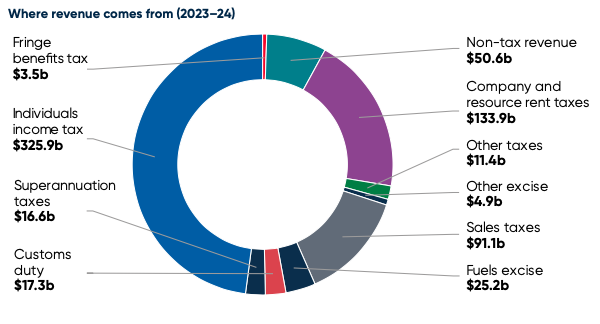

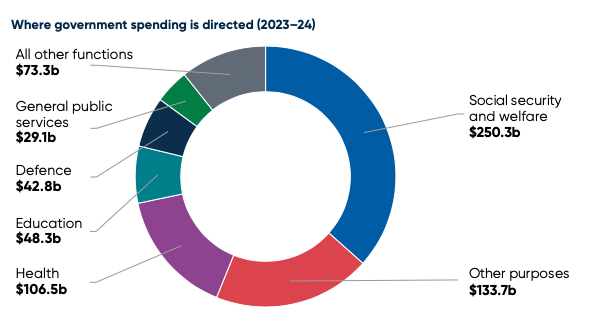

We provide you with a snapshot of the government’s revenue generation and spending. Total revenue for 2023–24 is expected to be $680.4 billion whereas total expenses are expected to be $684.1 billion.

COST OF LIVING, HEALTH CARE & COMMUNITY

Household energy bill relief

The Government is partnering with states and territories to offer up to $3 billion of direct energy bill relief to vulnerable households and small businesses.

With the Government’s other actions through the Energy Price Relief Plan, electricity bill increases are now expected to be around 25 percentage points smaller on average nationwide in 2023–24.

Strengthening Medicare

$5.7 billion will be provided over 5 years to strengthen Medicare.

This includes $3.5 billion to triple the bulk billing incentive for the most common GP consultations for children under 16 years, pensioners and other Commonwealth concession card holders.

The tripling of the bulk billing incentive applies to:

- all face‑to‑face and telehealth general practices services between 6 and 20 minutes long

- all other face‑to‑face general practice consultations

- longer telehealth and general practice consultations where a patient is registered with their regular practice through MyMedicare.

Cheaper child care and Paid Parental Leave

Effective 1 July 2023, around 1.2 million families will begin to benefit from cheaper child care. Child Care Subsidy rates will increase up to 90% for eligible families and up to 95% for any additional children in care aged 5 and under.

Expanding access to Parenting Payment (Single)

$1.9 billion will be invested across 5 years to expand eligibility for Parenting Payment (Single) to single principal carers until their youngest child turns 14. Around 57,000 eligible single parents, 91% women, will transition to a higher basic rate of $922.10 per fortnight. This is an increase of $176.90 per fortnight compared to current payments.

JobSeeker

Over 900,000 Australians on JobSeeker will get an extra $40 a fortnight.

That will take the fortnightly payment for a single person with no children to more than $730 a fortnight and will become a permanent increase.

The extra $40 a fortnight will also go to people on Youth Allowance, Austudy and other government payments.

Incentive to improve residential rental property supply

The Government has announced a series of measures to boost Australia’s rental stock:

- Increasing depreciation from 2.5% to 4% on new built-to-rent projects where construction commenced after 9 May 2023.

- Reducing the withholding tax rate from 30% to 15% for eligible fund payments from managed investment trusts to foreign residents on income from newly constructed residential build-to-rent properties after 1 July 2024 (subject to further consultation on eligibility criteria).

- Affordable housing through the National Housing Finance and Investment Corporation (NHFIC) – An additional $2bn has been allocated to the NHFIC, increasing the NHFIC’s cap from $5.5 billion to $7.5 billion from 1 July 2023 to support more social and affordable rental housing.

Indigenous Communities

Across 5 years, $1.9 billion will be spent on measures to improve the lives and economic opportunities available to Aboriginal and Torres Strait Islander people.

An additional $250 million will be spent improving community safety, services, education and job creation in Central Australia.

Access to home guarantee scheme expanded to friends and siblings

First Home Guarantee (FHG) – guarantees part of a first home owner’s home loan enabling the purchaser to acquire a home with as little as 5% deposit without paying Lenders Mortgage Insurance (LMI). The FHG is capped at 15% of the value of the property. 35,000 places are available to the scheme per year.

Current eligibility

Applying as an individual or couple (married / de facto)

- First-home buyers who have not previously owned, or had an interest in, a property in Australia.

- An Australian citizen(s) at the time they enter into the loan

- At least 18 years of age

- Earning up to $125,000 for individuals or $200,000 for couples, as shown on the Notice of Assessment (issued by the Australian Taxation Office)

- Intending to be owner-occupiers of the purchased property

Effective 1 July 2023

- Friends, siblings, and other family members will be eligible for joint applications not just an individual or couple (married de facto)

- First-home buyers and non-first-home buyers who haven’t owned a property in Australia in the last ten years

- Australian citizens and permanent residents at the time they enter the loan

- All other criteria remain the same

Regional First Home Buyer Guarantee – An extension of the FHG applicable to regional areas only. 10,000 places are available to the scheme each year to 30 June 2025.

Current eligibility

As above for the First Home Guarantee plus the borrower must have lived in the regional area (or adjacent) they are purchasing in for the preceding 12-month period to the date they execute the home loan agreement.

Effective 1 July 2023

As above for the FHG plus the regional area eligibility requirement.

Family Home Guarantee – guarantees the home loan of an eligible single parent with at least one dependent child enabling them to purchase a home with as little as 2% deposit without paying Lenders Mortgage Insurance. Guarantee capped at 15% of the value of the property. 5,000 places are available to the scheme each year to 30 June 2025.